We Found the Perfect Condo. Then We Read the HOA

You found it. The one with the view, the walkable neighborhood, the HOA that actually maintains things.

You call your agent — excited, ready to move. And the first thing she says is:

“Before we write this offer, we need to check if this building is warrantable.”

If you don’t know what that means yet, you’re about to. And it matters more than almost anything else in a condo purchase right now.

In 2021, a condominium in Surfside, Florida collapsed. Ninety-eight people died. The building had known structural issues. The HOA had been deferring maintenance for years.

In the aftermath, Fannie Mae and Freddie Mac — the two government-backed entities that together purchase the majority of U.S. conventional mortgages — rewrote their condo lending guidelines from the ground up. The new rules went into effect in 2022 and are now fully embedded in how every lender evaluates a condo purchase. What this means practically: before your lender can approve a conventional loan, they have to assess the building itself — not just you as a borrower.

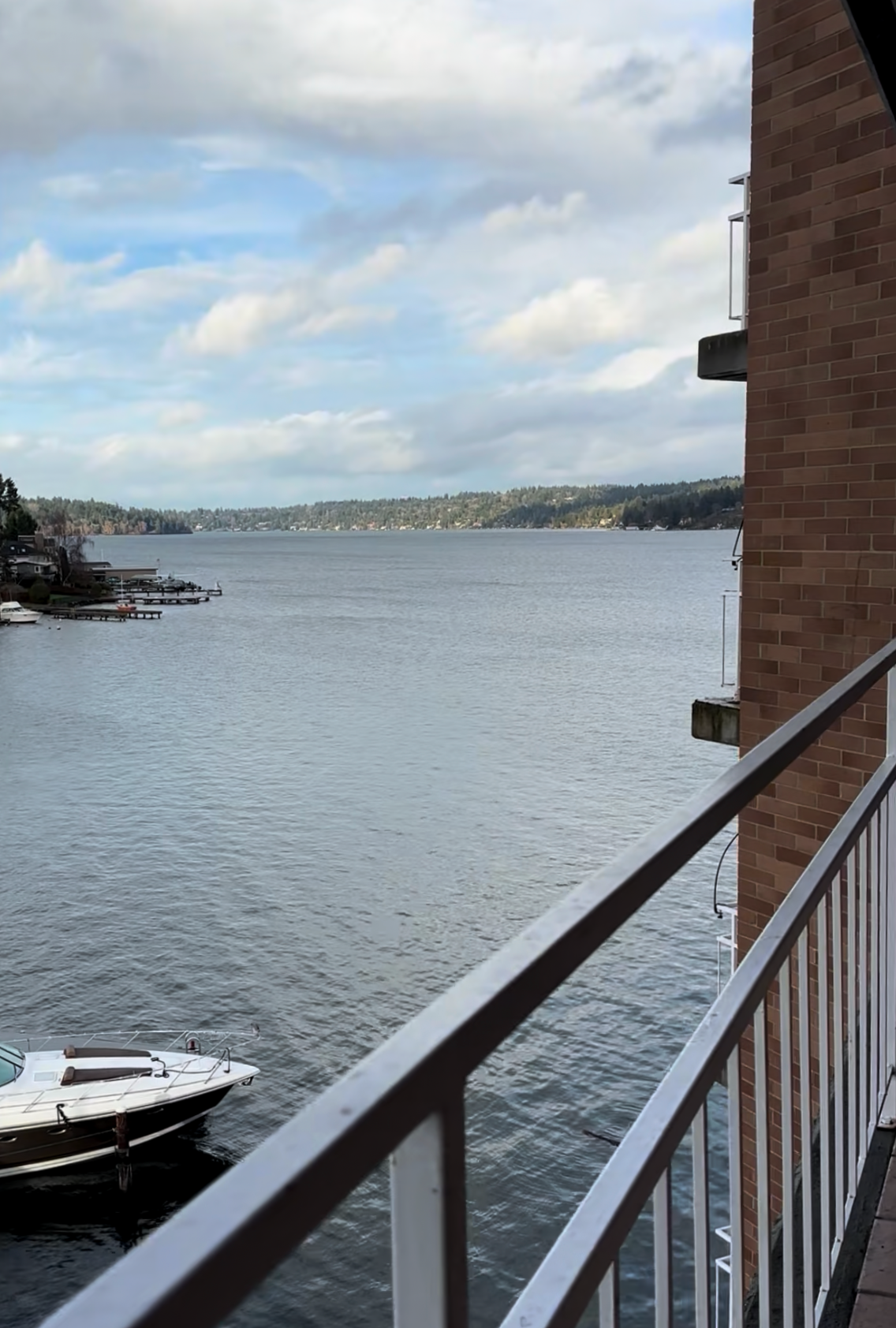

I think about a couple I worked with last year. They were looking for a second home — a quiet place, a retreat closer to their grandchildren. They found it in Madison Park, a small village on the edge of Lake Washington where you can walk to the Red Apple for groceries and feel, briefly, like the city doesn’t exist.

The building was built in the 1960s, long and low, stretching from the shore out over the lake on pylons. You can’t build that way anymore — tidewater laws have seen to it — which meant this was genuinely irreplaceable. Their unit was on the fourth floor. One bedroom, well-kept cabinets, a bathroom that had never been renovated but didn’t need to be. Neutral, quiet, tended.

Photo by TIA International Photography. Condo buildings like these are rare on Lake Washington.

The balcony was the star. You could sit out there and just listen to the waves.

They wanted it. Of course they wanted it.

But when the HOA documents came back, the picture changed. Galvanized metal pipes — aging infrastructure that would eventually need replacing. And reserves sitting right at 10%, the minimum threshold. Thin. The kind of thin that means one unexpected repair becomes everyone’s problem, fast.

Under today’s guidelines, a building like this would face serious scrutiny. Lenders now want to see reserves closer to 15% before issuing a conventional loan. Which means any future buyer would face the same wall — or worse.

We talked it through. They weren’t dramatic about it. The husband just said, quietly: we just don’t want to take on that risk. And they folded it into a kind of low disappointment, the kind that doesn’t make a scene but postpones something indefinitely.

They never did find another place like it.

What the New Rules Actually Require

The official term is “warrantability.” A warrantable condo meets Fannie Mae and Freddie Mac’s requirements — conventional loan, standard rates, standard terms. A non-warrantable condo means a portfolio loan, held by the bank rather than sold to the secondary market. Portfolio loans carry higher rates and typically require a larger down payment. That difference shows up in your monthly payment every single month.

Here’s what lenders are looking at when they evaluate a building:

Reserve funding. HOAs must allocate at least 10% of their annual budget to reserves — and in practice, lenders want to see closer to 15%. Reserves sitting at the bare minimum signal a building that can’t absorb the unexpected.

Delinquent dues. No more than 15% of unit owners can be behind on HOA dues. A building where too many people aren’t paying in is a building in quiet financial trouble.

Deferred maintenance. Known issues left unaddressed — especially anything touching safety, structure, or the building envelope — can disqualify a building from conventional financing outright.

Special assessments. These aren’t automatically disqualifying, but context matters. A building levying an assessment to repave the parking structure reads very differently than one responding to a structural emergency. Lenders will ask why.

Pending litigation. Active lawsuits involving the HOA — particularly anything related to safety or construction — can push a building outside conventional guidelines entirely.

The HOA questionnaire. Lenders now send a detailed document directly to the HOA. How quickly and completely the HOA responds can affect your closing timeline in ways that feel entirely outside your control — because they are.

A condo downtown, near pioneer square.

The biggest mistake buyers make is falling in love with a unit before anyone has checked the building. Ask early. A good listing agent should already know their building’s warrantability status. Get the HOA documents regardless — the reserve study, meeting minutes, and financial statements tell you not just whether you can get a loan, but how the building is being run and who you’d be sharing walls with.

If a building comes back non-warrantable, don’t automatically walk. Some buildings fall outside conventional guidelines for reasons that aren’t deal-breakers. Understand why before you decide. And work with a lender who knows condos — someone fluent in condo-heavy markets will spot issues before they become surprises at closing.

Here’s the thing nobody tells you upfront: buying a condo isn’t just buying a home. It’s buying into a community — a financial community, a maintenance community, a group of people who all have a stake in the same building. The new lending rules are really just a formal acknowledgment of something that was always true.

The building matters as much as the unit.

Find one that deserves you.

Questions about a building you're considering? I'm Xan — reach out. This is my favorite kind of conversation.